How Much Does IVF Cost? A Deep Dive into Fertility Treatment Expenses

April 1, 2025

What Is IVF? Your Complete Guide to In Vitro Fertilization

April 1, 2025How Much Is IVF with Insurance? Your Guide to Costs, Coverage, and More

How Much Is IVF with Insurance? Your Guide to Costs, Coverage, and More

In vitro fertilization (IVF) is a life-changing option for many people dreaming of starting a family. But if you’ve ever looked into it, you’ve probably noticed one big thing: it’s expensive. The good news? Insurance might help lighten the load—if you know how it works. So, how much does IVF really cost with insurance? Let’s break it down together, step by step, with all the details you need to feel confident and prepared.

IVF isn’t a one-size-fits-all journey, and neither are the costs. Whether insurance covers it, how much it covers, and what you’ll still pay out of pocket depend on a bunch of factors—like where you live, your insurance plan, and even your personal health situation. In this guide, we’ll dig into the numbers, share real-world examples, and give you practical tips to navigate it all. Plus, we’ll uncover some lesser-known angles that could save you money or stress along the way.

Ready to get started? Grab a coffee, and let’s dive in.

What Does IVF Cost Without Insurance?

Before we talk about insurance, it’s worth knowing what you’re up against if you’re paying for IVF out of pocket. The price tag can feel overwhelming, but understanding the baseline helps put everything else in perspective.

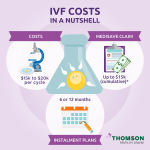

On average, one IVF cycle in the U.S. costs between $12,000 and $25,000. That’s a big range, right? Here’s why: the price depends on things like your location, the clinic you choose, and what extras your treatment includes. For example, a cycle in New York City or Los Angeles might hit the higher end—closer to $20,000 or more—while a smaller city might be nearer to $12,000. And that’s just the basics: monitoring, egg retrieval, lab work, and embryo transfer.

But wait, there’s more. Most people don’t get pregnant on their first try. Studies show the average patient needs 2 to 3 cycles to have a baby, which could push your total cost to $50,000 or even higher. Then there are add-ons like medications (another $3,000-$5,000 per cycle), genetic testing ($1,500-$3,000), or freezing embryos ($1,000-$2,000 plus storage fees). Suddenly, that “average” price starts climbing fast.

Here’s a quick breakdown of what you might pay without insurance:

- Base IVF cycle: $12,000-$25,000

- Medications: $3,000-$5,000

- Embryo freezing: $1,000-$2,000 (plus $300-$500/year for storage)

- Genetic testing (PGS/PGD): $1,500-$3,000

- Frozen embryo transfer (if needed): $3,000-$5,000

So, if you’re looking at multiple cycles with all the bells and whistles, you could easily be talking $60,000 or more. That’s where insurance comes in—or at least, where you hope it does.

Does Insurance Even Cover IVF?

Here’s the tricky part: not all insurance plans cover IVF. In the U.S., fertility treatments are often seen as “elective,” meaning many insurance companies don’t automatically include them. But it’s not all bad news. Some states and employers are stepping up, and coverage is getting better—slowly.

As of April 2025, 20 states have laws requiring some level of infertility coverage for state-regulated insurance plans. Ten of these states—like Massachusetts, New York, and Illinois—have what’s called “comprehensive” IVF mandates. That means they require insurance to cover IVF with fewer restrictions, like age limits or lifetime caps. For example, Massachusetts covers unlimited cycles (yep, unlimited!), while New York caps it at three.

But there’s a catch: these mandates only apply to certain plans. If your employer self-funds their insurance (common with big companies), they’re exempt from state rules. About 61% of workers with employer-sponsored plans fall into this category, according to the Kaiser Family Foundation. So, even if you live in a mandate state, your plan might not cover IVF unless your employer opts in.

Federal employees got a boost recently, though. In 2023, the U.S. Office of Personnel Management expanded fertility benefits for nearly 9 million people, including coverage for up to three IVF cycles per year starting in 2024. Military families under TRICARE and veterans through the VA also have some options, but only in specific cases—like if infertility stems from a service-related injury.

So, does your insurance cover IVF? You’ll need to check your plan. Look for terms like “infertility treatment,” “assisted reproductive technology,” or “IVF” in your policy docs. Or better yet, call your insurance provider and ask directly. It’s a hassle, but it’s worth it.

How Much Is IVF with Insurance?

Okay, let’s get to the big question: how much will IVF cost if you do have insurance? The answer depends on your coverage, but here’s what you can expect.

Full Coverage Plans

If you’re lucky enough to have a plan that fully covers IVF—like some folks in mandate states or with generous employers—the out-of-pocket cost can drop to almost nothing. For example, in Massachusetts, where insurance must cover unlimited cycles, patients might only pay co-pays ($20-$50 per visit) or a small deductible (say, $500-$1,000). Total cost? Maybe $1,000-$2,000 per cycle, tops.

A real-life example: Sarah, a 34-year-old teacher in Boston, told me her insurance covered three cycles fully after a $500 deductible. Her total cost, including meds, was under $2,000. Compare that to $50,000 without insurance—huge difference.

Partial Coverage Plans

More common are plans that cover parts of IVF. Maybe they pay for monitoring and egg retrieval but not the lab work or meds. Or they cap coverage at a dollar amount, like $10,000 lifetime. In these cases, your cost might look like this:

- Base cycle: $12,000 (insurance covers $8,000, you pay $4,000)

- Meds: $4,000 (not covered, all on you)

- Extras: $2,000 (genetic testing or freezing, usually out of pocket)

Total per cycle? Around $10,000-$12,000, depending on what’s covered. Still a lot, but better than $20,000.

No IVF Coverage, But Some Benefits

Even if your plan doesn’t cover IVF itself, it might cover related stuff—like diagnostic tests (bloodwork, ultrasounds) or fertility drugs. This can shave $1,000-$3,000 off your bill. For instance, a friend in Texas had no IVF coverage but got her $4,000 medication bill cut in half thanks to her plan’s prescription benefits.

Here’s a handy table to compare:

| Scenario | Total Cost per Cycle | What You Pay |

|---|---|---|

| Full coverage | $12,000-$25,000 | $500-$2,000 |

| Partial coverage | $12,000-$25,000 | $8,000-$12,000 |

| No IVF coverage | $12,000-$25,000 | $12,000-$25,000 |

Your actual cost? Call your insurance and crunch the numbers. It’s the only way to know for sure.

What Affects Your IVF Costs with Insurance?

Even with insurance, IVF isn’t a flat rate. Here are the big factors that can shift your bill up or down.

Where You Live

Location matters—a lot. States with mandates (like California or New Jersey) often have lower out-of-pocket costs because insurance picks up more of the tab. But in states like Florida or Arizona, with no mandates, you’re more likely to pay full price unless your employer steps in. Clinics in big cities also tend to charge more due to higher overhead.

Your Insurance Plan

Self-funded plans (exempt from state rules) are a wild card. Some cover IVF anyway—think big tech companies like Google, which offers up to $75,000 in fertility benefits. Others? Nada. Check your employer’s benefits package or ask HR.

Your Treatment Plan

IVF isn’t just one procedure. If you need extras—like ICSI (injecting sperm directly into the egg) or donor eggs—costs climb. Insurance might cover the basics but not these add-ons. For example, donor eggs can add $15,000-$20,000, and most plans won’t touch that.

Number of Cycles

Success rates vary by age. If you’re under 35, you’ve got a 40-50% chance of a live birth per cycle, per the CDC. Over 40? It drops to 10-15%. More cycles mean more money, even with insurance. Some plans cap cycles at 2 or 3; others stop at a dollar amount. Know your limit.

Hidden Costs Insurance Might Not Cover

Insurance can help, but it doesn’t catch everything. Here are some sneaky expenses to watch for:

- Travel: If the best clinic is hours away, gas, flights, or hotels add up.

- Time off work: Appointments are frequent, and unpaid leave can hit your wallet.

- Emotional support: Therapy or counseling (common during IVF) isn’t usually covered.

- Storage fees: Frozen embryos cost $300-$500 per year to store, often out of pocket.

One couple I spoke to spent $1,500 on travel and lodging for a top clinic two states away. Insurance didn’t cover a dime of that.

Interactive Quiz: What’s Your IVF Cost Range?

Wondering where you might land? Take this quick quiz to get a ballpark idea. Answer yes or no, and tally your points.

- Do you live in a state with an IVF mandate? (Yes = 2 points, No = 0)

- Does your insurance explicitly cover IVF? (Yes = 3 points, No = 0)

- Are you under 35? (Yes = 1 point, No = 0)

- Does your plan cover medications? (Yes = 2 points, No = 0)

Score:

- 7-8 points: Likely $1,000-$5,000 per cycle (great coverage, good odds)

- 4-6 points: Around $5,000-$10,000 (some help, but gaps remain)

- 0-3 points: $12,000-$25,000 (little to no coverage, full cost)

This isn’t exact, but it’s a starting point. Chat with your insurer for the real scoop.

How to Lower Your IVF Costs with Insurance

Paying less sounds good, right? Here are some practical ways to make it happen.

Maximize Your Coverage

- Ask for pre-authorization: Some plans need approval before covering IVF. Get it in writing.

- Use in-network clinics: Out-of-network care might not be covered—or cost more.

- Split billing: If meds aren’t covered, see if your pharmacy plan can help separately.

Look Beyond Insurance

- Fertility grants: Groups like BabyQuest offer up to $15,000 for treatment. Apply early—funds run out fast.

- Clinic discounts: Some offer multi-cycle packages (e.g., $25,000 for 3 cycles) or refunds if you don’t conceive.

- Medicare savings: In rare cases, if infertility ties to a medical condition (like cancer treatment), Medicare might pitch in.

Shop Around

Clinic prices vary. A 2023 study from Stanford found costs differ by up to 30% within the same city. Call around, ask for itemized quotes, and compare.

The Latest Trends in IVF Coverage (April 2025)

IVF is a hot topic right now, and things are shifting fast. Here’s what’s new based on recent chatter and data.

State Laws Are Evolving

California just passed a law in late 2024 requiring insurance to cover IVF starting in 2025. X posts show mixed feelings—some cheer the access, others worry premiums will spike. It’s too early for hard numbers, but expect costs to spread across policyholders, potentially raising rates by 1-2%.

Employers Are Stepping Up

Big companies like Amazon and Starbucks now offer IVF benefits—up to $25,000 or more. A 2024 Mercer survey found 42% of large employers cover some IVF, up from 27% in 2021. If you work for a smaller firm, ask HR to consider it—employee demand is driving change.

Public Funding Experiments

British Columbia launched a public IVF program in 2024, offering one cycle (up to $19,000) to residents. Could the U.S. follow? Some states, like Nebraska, are floating bills to cover IVF for state employees. It’s a long shot, but worth watching.

Three Things You Haven’t Heard About IVF Costs

Most articles stick to the basics—price, coverage, done. But there’s more to the story. Here are three angles you won’t find everywhere.

1. Racial Disparities in Access Persist

Even with insurance, not everyone benefits equally. A 2019 study in Reproductive Biology and Endocrinology found Black and Hispanic women use IVF less than White women, even in mandate states. Why? Higher dropout rates after failed cycles, cultural barriers, and income gaps. Insurance helps, but it’s not the whole fix. Clinics could do more—like offering sliding-scale fees or outreach programs.

2. The Emotional Cost Adds Up

Money isn’t the only price. IVF takes a toll—stress, hope, disappointment. A 2023 Swedish study found couples without insurance faced worse mental health outcomes due to financial strain. Therapy can help (around $100-$200/session), but it’s rarely covered. Budget for this—it’s as real as the medical bills.

3. Overseas IVF Is Cheaper—But Risky

Some folks head abroad to save cash. A cycle in Mexico or Spain might cost $5,000-$8,000, half the U.S. price. Insurance won’t cover it, and quality varies. A 2024 X thread warned of clinics cutting corners—think fewer tests or rushed transfers. Research heavily if you’re tempted.

Real Stories: IVF Costs in Action

Numbers are one thing; people are another. Here’s how IVF costs played out for three families.

Mia, 29, Illinois

Mia’s insurance covered two cycles after a $1,000 deductible. Meds were partially covered ($1,500 out of $4,000). Total per cycle? About $3,500. She got pregnant on her second try—grand total: $7,000. “Way less than I feared,” she said.

Jake and Lisa, 38, Florida

No mandate state, no coverage. Their clinic charged $18,000 per cycle, plus $4,000 for meds. After two cycles and no baby, they’re out $44,000. “We’re tapped out,” Jake admitted. They’re now exploring grants.

Priya, 42, California

Priya’s employer offered $20,000 in benefits. One cycle with donor eggs cost $30,000—insurance covered most, leaving her with $10,000 out of pocket. She’s expecting twins soon. “Worth every penny,” she smiled.

Your IVF Cost Checklist

Ready to figure out your own costs? Use this step-by-step guide:

✔️ Step 1: Check your state

Look up if you’re in a mandate state (Google “IVF mandate [your state]”).

✔️ Step 2: Review your plan

Call your insurance. Ask: “Do you cover IVF? What’s my deductible? Are meds included?”

✔️ Step 3: Talk to clinics

Get quotes from 2-3 local clinics. Ask for a breakdown—base cost, meds, extras.

✔️ Step 4: Plan for extras

Budget for travel, time off, or storage fees.

✔️ Step 5: Explore help

Research grants, discounts, or financing (some clinics offer 0% interest loans).

Poll: What’s Your Biggest IVF Worry?

Let’s hear from you! Vote below and see what others think—it only takes a sec.

- A: The cost, even with insurance

- B: Whether insurance will cover enough

- C: Success rates and multiple cycles

- D: Hidden fees or unexpected bills

Drop your pick in the comments—I’ll tally the results next week!

{kind=link}