What Is IVF? Your Complete Guide to In Vitro Fertilization

April 1, 2025

How Does IVF Work? A Deep Dive into the Journey of In Vitro Fertilization

April 1, 2025Does Insurance Cover IVF? Your Guide to Understanding Fertility Treatment Costs

Does Insurance Cover IVF? Your Guide to Understanding Fertility Treatment Costs

Navigating the world of fertility treatments can feel overwhelming, especially when you’re hit with the big question: Does insurance cover IVF? If you’re dreaming of starting a family but facing infertility, you’re not alone—about one in eight couples in the U.S. deals with this challenge. In vitro fertilization (IVF) is a game-changer for many, but the costs can be jaw-dropping. So, let’s break it down together. This guide will walk you through what insurance might cover, why it varies so much, and how you can figure out your options—all in a way that’s easy to digest and packed with practical tips.

What Is IVF, and Why Does It Matter?

IVF stands for in vitro fertilization, a process where doctors take eggs from the ovaries, fertilize them with sperm in a lab, and then place the resulting embryos into the uterus. It’s often a lifeline for people who can’t conceive naturally due to issues like blocked fallopian tubes, low sperm count, or unexplained infertility. For some, it’s also a path to parenthood for same-sex couples or single individuals using donor eggs or sperm.

The catch? IVF isn’t cheap. A single cycle can cost anywhere from $12,000 to $20,000 in the U.S., not counting medications, which tack on another $3,000 to $5,000. That’s why insurance coverage—or the lack of it—can make or break someone’s decision to pursue it. Understanding what’s covered is the first step to making this journey less stressful.

The Basics of Insurance and IVF: What You Need to Know

Here’s the short version: insurance coverage for IVF depends on where you live, who your employer is, and what plan you have. Unlike routine doctor visits or maternity care, fertility treatments aren’t always seen as “essential” by insurance companies. Some plans cover it fully, others partially, and many don’t cover it at all. Let’s unpack this.

Why Coverage Isn’t Guaranteed

Insurance companies often classify IVF as an elective procedure, not a medical necessity. Think of it like getting braces—some plans cover orthodontics for kids, but not always for adults. Similarly, infertility is sometimes viewed as a “lifestyle choice” rather than a health condition, even though the World Health Organization calls it a disease. This mindset shapes what’s covered and what’s not.

The Role of State Laws

Where you live plays a huge role. As of April 2025, 21 states in the U.S. have laws requiring some level of infertility treatment coverage. These are called “mandates,” and they vary wildly:

- Comprehensive Mandates: States like Massachusetts, New Jersey, and Illinois require insurance to cover multiple IVF cycles with few restrictions. For example, Massachusetts covers unlimited cycles for eligible patients.

- Limited Mandates: States like Texas or Arkansas might cover diagnostics (like blood tests) but not IVF itself—or they’ll only cover it if you use your spouse’s sperm.

- No Mandates: If you’re in a state like Florida or Alabama, you’re mostly on your own unless your employer opts in.

Even in mandate states, there’s a catch: these laws usually only apply to companies with more than a certain number of employees (often 50 or 100). Plus, if your employer “self-insures” (pays claims directly instead of buying a full insurance plan), they can skip these rules entirely.

Employer Plans Make a Difference

If you get insurance through your job, your coverage depends on what your employer chooses. Big companies like Google or Starbucks often offer generous fertility benefits—sometimes covering up to $20,000 or more for IVF—to attract talent. Smaller businesses might not. A 2021 Mercer survey found that only 27-42% of employer-sponsored plans include IVF coverage, even though more are starting to add it in a tight job market.

How to Check If Your Insurance Covers IVF

Wondering about your own plan? Don’t guess—dig in. Here’s a step-by-step guide to figure it out:

- Read Your Policy: Grab your insurance booklet or log into your online portal. Look for sections on “infertility,” “fertility treatments,” or “assisted reproductive technology.” Words like “IVF” or “exclusions” are your clues.

- Call Your Insurance Provider: Dial the number on your card and ask: “Does my plan cover IVF? What about medications or diagnostics?” Take notes—get the rep’s name and date of the call in case you need to follow up.

- Talk to HR: If you’re on an employer plan, your human resources team can clarify what’s included. Ask about lifetime maximums (like $15,000) or cycle limits (like three rounds of IVF).

- Check State Laws: Google “infertility insurance mandate [your state]” to see if there’s a law backing you up. Sites like RESOLVE (resolve.org) have handy state-by-state breakdowns.

✔️ Pro Tip: Ask about “pre-authorization.” Some plans require you to prove you’ve tried cheaper options (like fertility drugs) before they’ll cover IVF.

❌ Watch Out: Don’t assume “infertility coverage” means IVF—some plans only pay for tests, not treatments.

What’s Typically Covered (and What’s Not)

Even if your insurance covers IVF, it’s rarely a blank check. Here’s what you might see:

Covered Costs

- Diagnostics: Blood tests, ultrasounds, or semen analysis to figure out why you’re not conceiving.

- Medications: Drugs to stimulate egg production (like Clomid or injectables), though coverage varies.

- IVF Procedures: Egg retrieval, lab fertilization, and embryo transfer—sometimes up to a set number of cycles.

- Freezing: Some plans cover cryopreservation (storing embryos) for future use.

Not Covered (Usually)

- Donor Eggs or Sperm: If you need a donor, you’re often paying out of pocket—$1,000 to $3,000 per donor cycle.

- Surrogacy: Most plans won’t touch this; it’s a separate beast costing $100,000+.

- Extra Services: Things like genetic testing of embryos (PGT) or intracytoplasmic sperm injection (ICSI) might be excluded.

Real-Life Example

Take Sarah, a 34-year-old teacher in New York. Her state mandates three IVF cycles for large-group plans. Her insurance covered her egg retrieval and transfer, but she had to pay $4,000 for meds because her plan capped drug coverage at $2,000 per cycle. Meanwhile, her friend Mike in Georgia got zero coverage—his employer opted out of fertility benefits entirely.

Why Coverage Varies So Much: The Hidden Factors

Ever wonder why your cousin in California gets full IVF coverage while you’re stuck with nothing? Here’s what’s behind the chaos:

State Mandates Aren’t Equal

Even in mandate states, rules differ. New York’s law covers three cycles but excludes same-sex couples unless they’ve tried insemination first. Arkansas demands you use your husband’s sperm—tough luck if that’s not an option. These quirks mean coverage isn’t one-size-fits-all.

Employer Size and Choices

Big corporations with self-insured plans (think Walmart or Amazon) can dodge state mandates. Smaller companies might not have the budget to add IVF benefits. It’s a roll of the dice based on where you work.

Insurance Plan Tiers

Basic plans might skip IVF, while premium ones include it. If you’re picking during open enrollment, compare options carefully—saving $50 a month on premiums could cost you thousands in uncovered treatments.

Public Opinion and Politics

Trending discussions on X show a split: some see IVF as a right everyone should access, while others argue it’s too expensive to mandate. In 2024, political promises—like Trump’s pledge to make insurance cover IVF—stirred debate, but no federal law exists yet. A 2021 study in Fertility and Sterility Reports found 55% of Americans support private insurance covering IVF, especially for medical infertility—not so much for elective cases.

Interactive Quiz: Does Your Insurance Cover IVF?

Let’s make this fun. Answer these quick questions to get a sense of your situation:

- Do you live in a state with an infertility mandate? (Check RESOLVE’s list!)

- A) Yes

- B) No

- Is your insurance through a big employer (100+ employees)?

- A) Yes

- B) No

- Does your plan mention “fertility treatments” or “IVF” in the benefits?

- A) Yes

- B) No

Results:

- Mostly A’s: Good news—you’re more likely to have some coverage!

- Mostly B’s: Hmm, you might be paying out of pocket unless your employer steps up.

No matter your score, call your insurer to confirm. Plans change, and exceptions pop up!

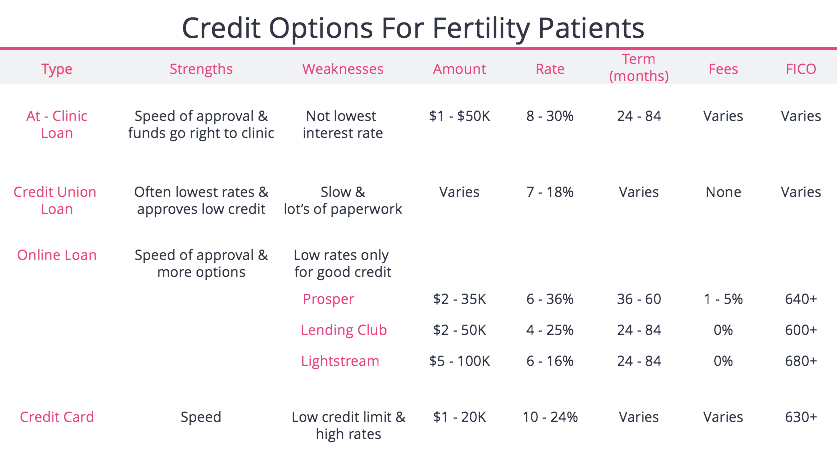

Beyond Insurance: Creative Ways to Pay for IVF

If insurance lets you down, don’t lose hope. People get creative every day. Here are some options:

Financing Programs

- Clinics: Many offer payment plans or refund programs. For example, “CareShare” at RMA Network refunds you if six IVF cycles fail.

- Loans: Companies like Future Family or CapexMD provide fertility-specific loans with lower interest rates than credit cards.

Grants and Scholarships

Nonprofits like BabyQuest or the Tinina Q. Cade Foundation award grants—sometimes up to $10,000—for IVF. Apply early; spots fill fast.

Crowdfunding

Sites like GoFundMe let you share your story and ask friends or strangers for help. One couple raised $15,000 this way after posting a heartfelt video.

Savings or HSAs

Got a Health Savings Account? IVF costs qualify. Dip into savings if you can—it’s an investment in your future family.

✔️ Pro Tip: Combine methods. A grant might cover meds, while a loan handles the procedure.

❌ Watch Out: Avoid high-interest credit cards—they’ll haunt you long after treatment ends.

The Emotional Side: Coping When Coverage Falls Short

Let’s be real: finding out IVF isn’t covered can hit hard. You might feel angry, helpless, or stuck. Sarah, our teacher from earlier, cried for days when her first cycle failed, and insurance wouldn’t fund a second try. But she regrouped, researched grants, and leaned on a support group.

Try this:

- Talk It Out: Join an online forum like FertilityIQ or a local RESOLVE group.

- Budget Smart: Focus on one step at a time—maybe start with diagnostics, then save for treatment.

- Celebrate Wins: Even a covered ultrasound is progress.

New Research: What’s Changing in 2025

IVF coverage is evolving. Here’s what’s fresh as of April 2025:

Employer Trends

A KFF report from late 2024 found more companies adding IVF benefits—up to 45% of large firms—thanks to employee demand and a competitive job market. Tech giants like Meta now cover $25,000+ per employee.

State Updates

Colorado joined the mandate club in 2024, requiring three IVF cycles for large plans starting January 2025. Advocates hope this sparks a domino effect.

Success Rates and Costs

A 2023 CDC study showed IVF live birth rates hit 52% per cycle for women under 35—up from 25% in 1995. Better tech means fewer cycles, but costs keep climbing with inflation. Medications alone rose 10% since 2020, per ASRM data.

Unique Angle: The Hidden Costs of “Partial Coverage”

Most articles gloss over this, but partial coverage can be a trap. Imagine your plan covers egg retrieval but not meds. You’re still shelling out thousands mid-cycle, derailing your budget. Or say it covers three cycles—but only if you’ve failed three IUIs (intrauterine inseminations) first. That’s months of delay and extra costs ($1,000-$2,000 per IUI).

Case Study: Lisa in Illinois had “great” coverage—three cycles included. But her plan required six months of fertility drugs first, costing her $1,200 out of pocket. By the time IVF started, she was exhausted and $5,000 poorer than expected.

Fix It: Ask your insurer for a full cost breakdown before you start. Get every detail in writing.

IVF Around the World: A Fresh Perspective

The U.S. lags behind other countries in IVF coverage. In France, the government funds up to six cycles if you’re under 43. Israel covers unlimited attempts until you have two kids. Even Canada’s provinces chip in—Ontario offers one cycle for free. Why the gap? America’s private insurance system prioritizes profit over universal care, leaving gaps no other developed nation tolerates.

Could this change? With 69% of Americans supporting coverage for medical infertility (per a 2024 Gallup poll), pressure’s building. Keep an eye on 2026 elections—federal mandates might finally hit the table.

Interactive Checklist: Your IVF Funding Plan

Ready to take charge? Use this checklist to map your next steps:

- Call my insurance to confirm IVF coverage details.

- Research my state’s mandate laws on RESOLVE.org.

- Ask HR about employer benefits or upcoming plan changes.

- Explore one grant (e.g., BabyQuest) and apply by next month.

- Get a clinic quote for out-of-pocket costs if insurance falls short.

Tweak it as you go—every box checked is a win!

The Bigger Picture: Is IVF Coverage a Right?

Here’s a thought to chew on: should IVF be covered like cancer treatment or childbirth? Supporters say infertility’s a medical condition—why treat it differently? Critics argue it’s too costly for insurers to handle universally; the Cato Institute pegged a federal IVF program at $7 billion yearly.

What do you think? Some X users call it a “human right,” while others say it’s a luxury. The truth probably lies in between—but until policy catches up, you’re left navigating this patchwork system.

Wrapping Up: Your Path Forward

So, does insurance cover IVF? Sometimes yes, sometimes no—it’s a maddening mix of state rules, employer choices, and plan fine print. But you’ve got tools now: check your coverage, explore alternatives, and lean on new trends like rising employer benefits or state expansions. Whether it’s a grant, a loan, or a lucky insurance win, there’s a way forward.

You’re not just chasing a baby—you’re building a future. Take it one step at a time, and don’t be afraid to ask for help. What’s your next move? Maybe it’s that phone call to your insurer—or a chat with a friend who’s been there. Whatever it is, you’ve got this.

{kind=link}